Patchy economic recovery continues

Indicators shows Bangladesh industrial production, exports, imports and tax revenues on the rise – but impact of delta variant yet to be seen.

This is the third edition of our set of 18 charts about the Bangladesh economy, with three months of further data.

For more about the purpose and background of the charts and about the significance of each indicator, read the first article in March here. You can also read the second set of charts published in June here.

The first two instalments, in March and June, confirmed the anecdotal evidence that at least the urban and formal sectors of the economy ground to a halt in 2020, and were yet to show any signs of durable recovery in early 2021. Further, these indicators contradicted the official GDP growth estimates of 5.2% in 2019-20 and 6.1% in 2020-21 (In Bangladesh, financial years are from July 1st to June 31st)

In August, the Bangladesh Bureau of Statistics revised down the official GDP growth figures for both financial years. Chart A shows that the economic growth in 2019-20 was the slowest since the late 1980s. This sharp economic slowdown is consistent with the indicators considered in this series.

The picture for 2020-21, however, is more mixed. According to the revised national accounts, at least a partial economic recovery did take place in that year. Indeed, the indicators considered in our series also point to a recovery, albeit patchy and uneven across different sectors, in the summer of 2021. However, neither the partial indicators nor the BBS GDP figures fully take into account the economic impact of the delta variant. The December update of this series should shed more light on this.

Finally, it should be noted that the indicators only represent the urban, formal economy, and not the rural, agricultural, and the informal sectors. While it’s hard to see the informal sector thriving when the formal economy is sluggish, the lack of any explicit indicator of the agriculture sector presents an important caveat to the analysis presented.

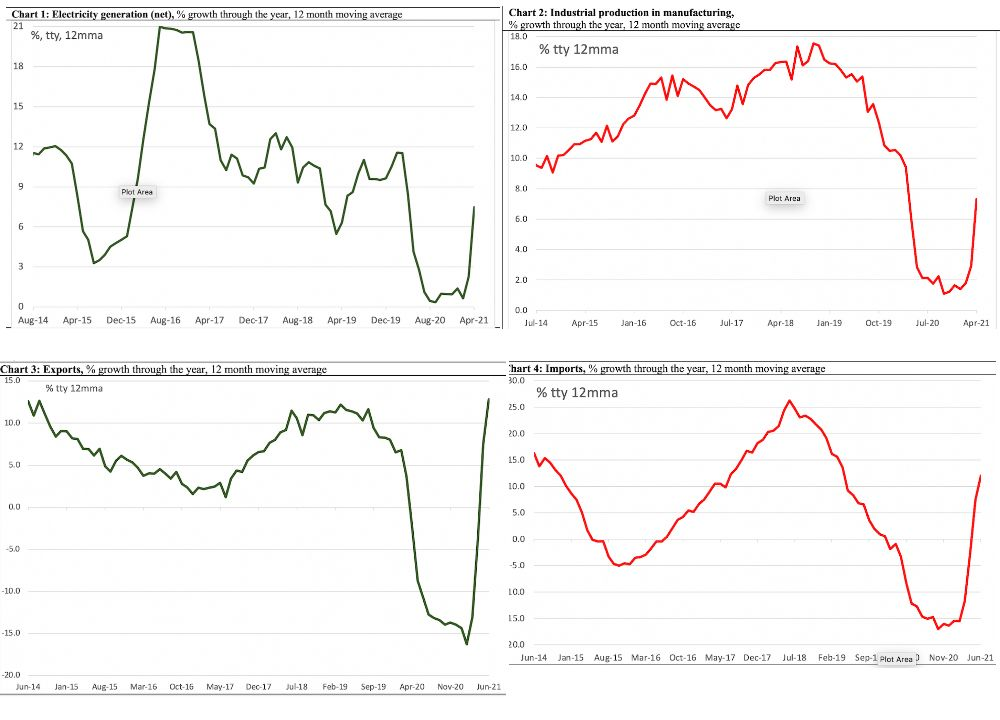

Chart 1: Electricity Generation

Prior to COVID-19, electricity generation was growing by 9-11% a year. After stagnating for nearly a year, it grew by 1.4% in the year to January 2021 and by 7.5% in the year to April 2021, pointing to an economic recovery.

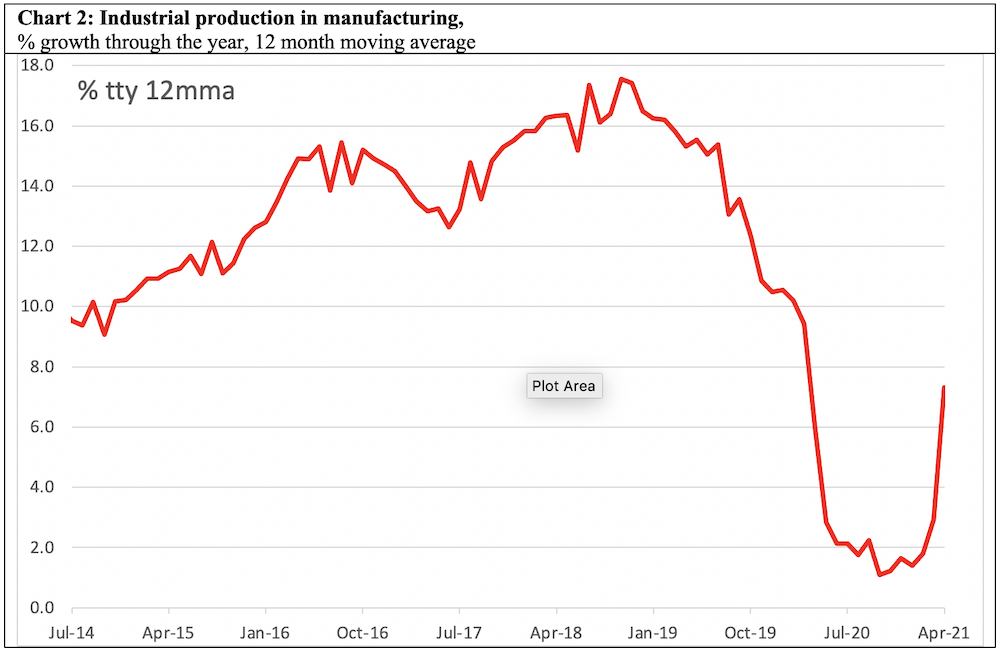

Chart 2: Industrial production

After nearly a year of stagnation, and growing by only 1.4% in the year to January 2021, it has staged a recovery in April 2021 growing by 7.3% in the year to April 2021.

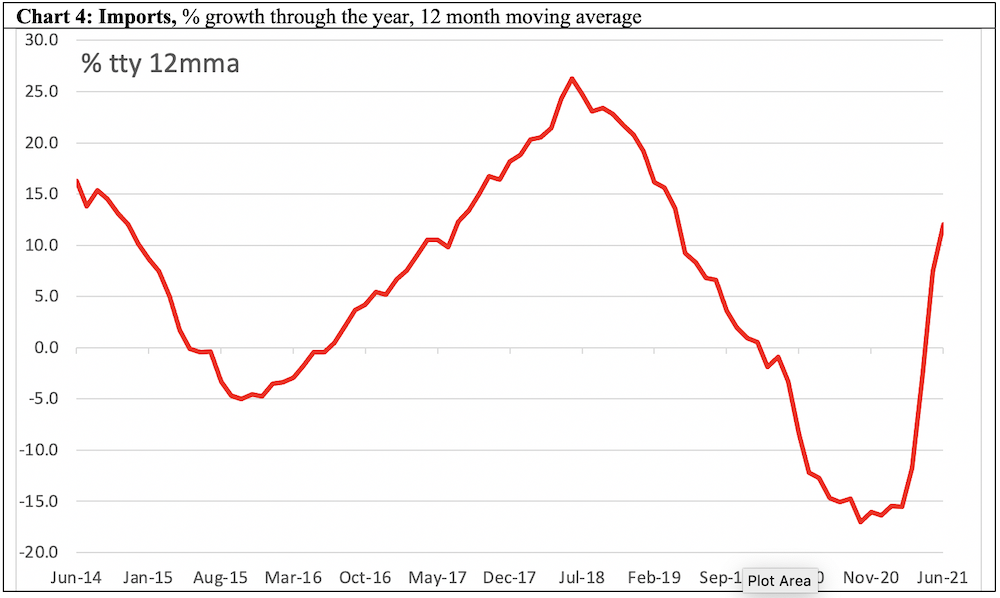

Chart 3: Exports

Exports continue to make a healthy recovery, growing by 12.8% in the year to June 2021.

Chart 4: Imports

Imports also continue to stage a healthy recovery in the summer of 2021 growing by 12% in the year to June 2021.

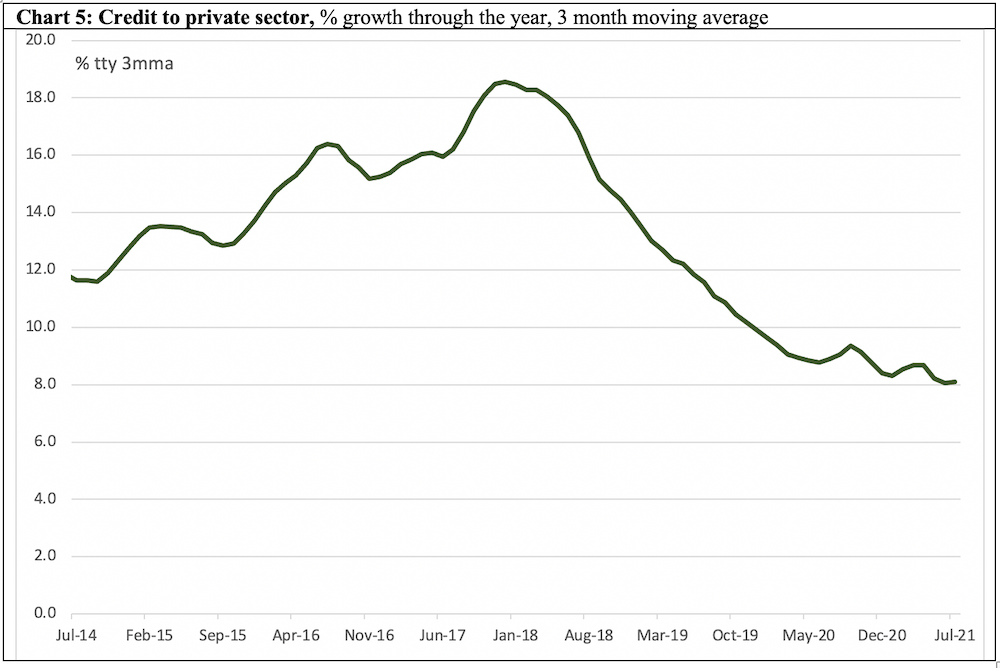

Chart 5 Credit to private sector

Growth in credit to private sector started slowing in 2018, well before the pandemic, and — as was the case three months ago — it was yet to clearly bottom out as of July 2021.

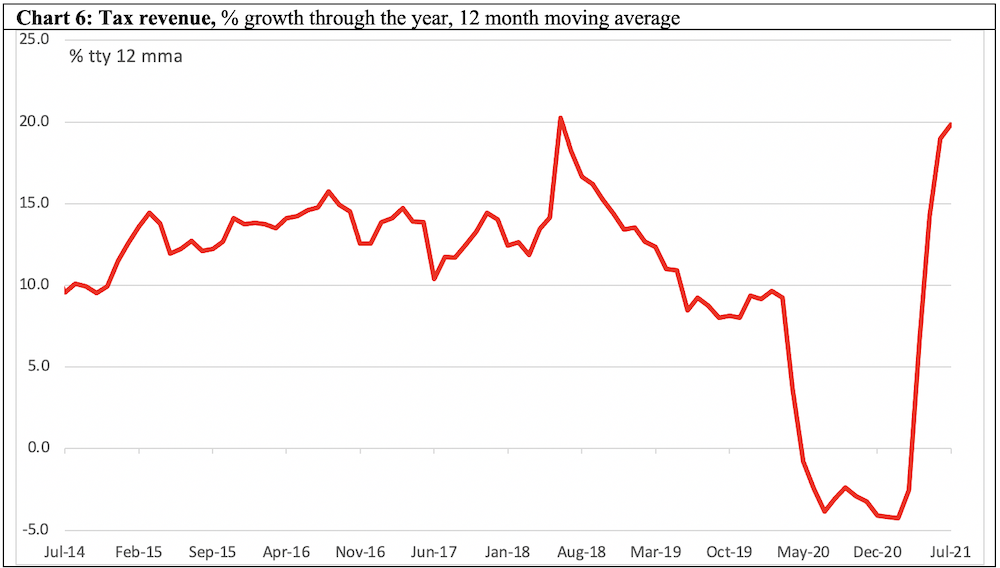

Chart 6: Tax revenue

Tax revenue had grown by nearly 7% in the year to April 2021, and it continued to grow in the year to July 2021 by 19%. Strong growth in tax revenue is consistent with the recovery seen in some of the other indicators.

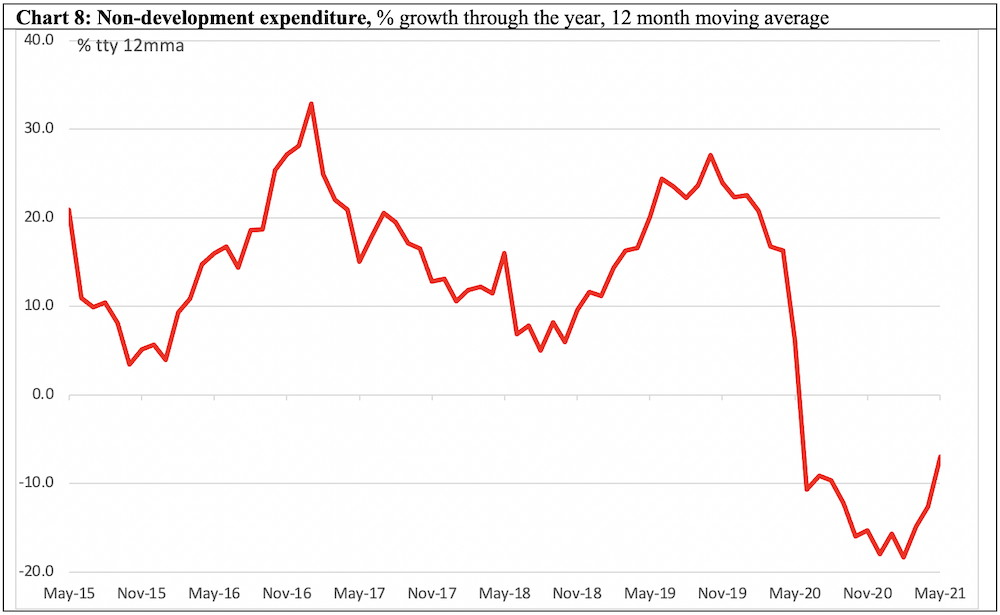

Charts 7 and 8: Development and non-development expenditure

Both collapsed during the lockdown, and similarly to three months ago, neither appeared to have staged a recovery as of May 2021 – though there are signs of a small turnaround.

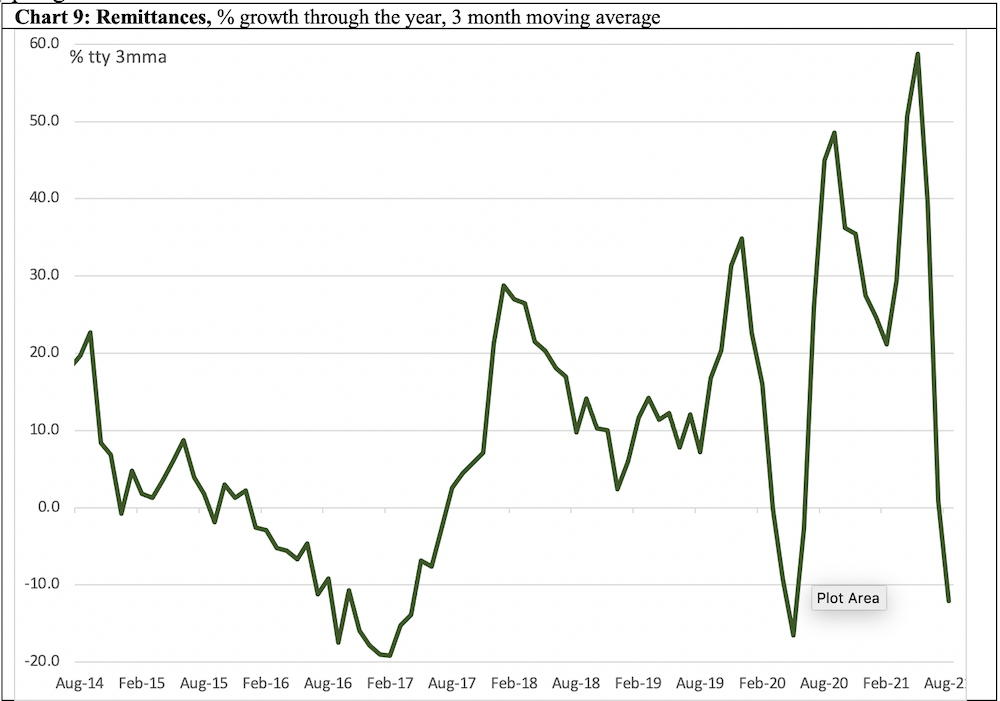

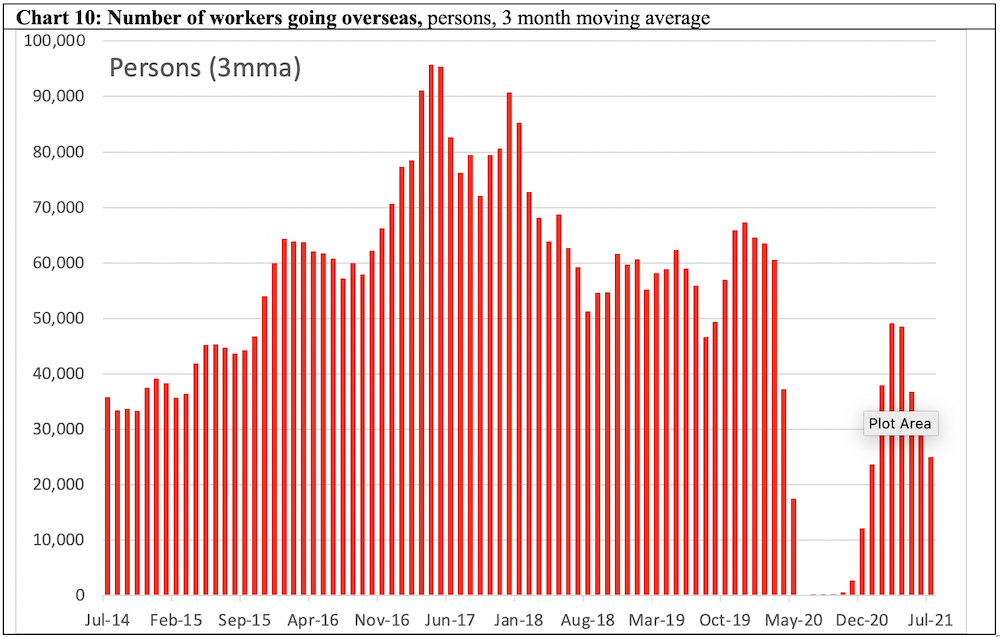

Charts 9 and 10: Remittances and Overseas Workers

In April 2021, remittances had sharply increased, but the onset of the delta variant outbreak resulted in renewed decline in remittances in the year to August 2021. The delta outbreak has also dampened the recovery in workers going overseas that had started in the spring of 2021.

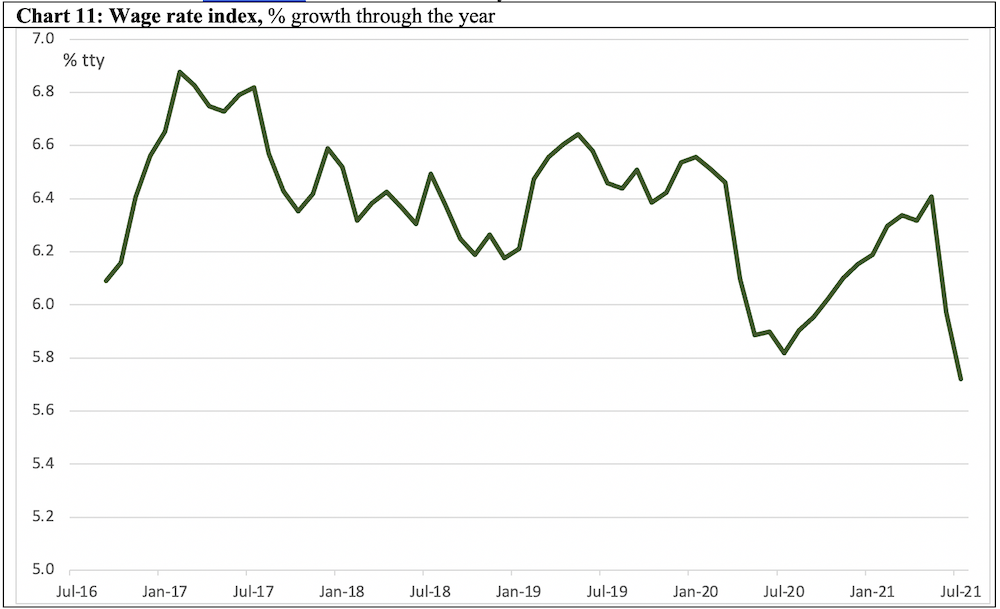

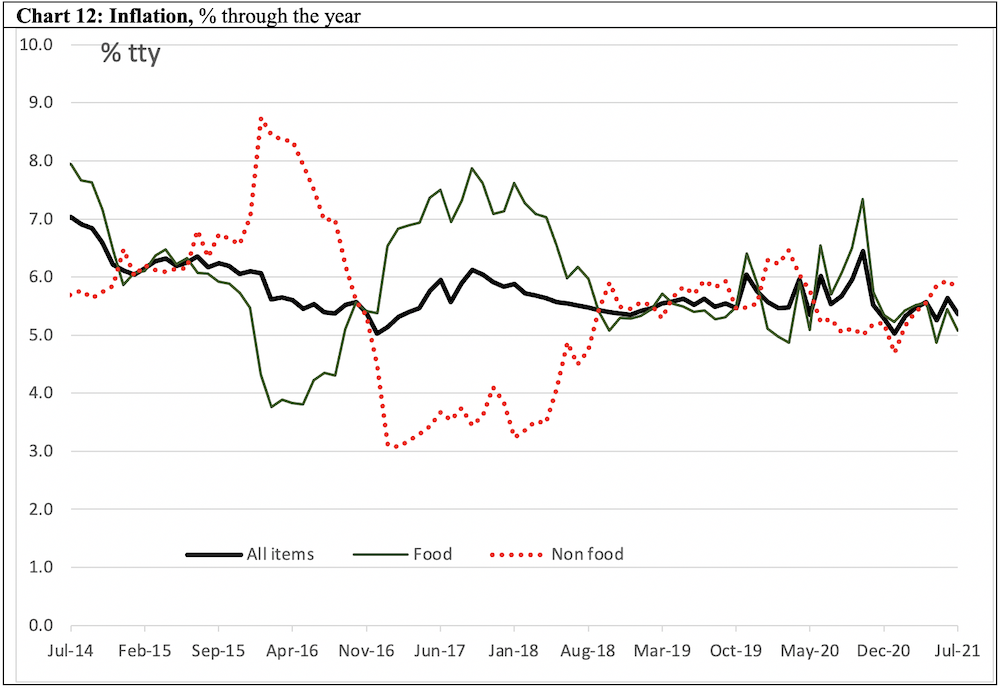

Charts 11 and 12: Wage rate index and inflation

Wage rates had grown by 6.4% in the year to May 2021 but with the onset of the delta variant in mid‑2021, the growth in wage rates slowed sharply as of August 2021. Inflation continues to remain moderate as of July 2021.

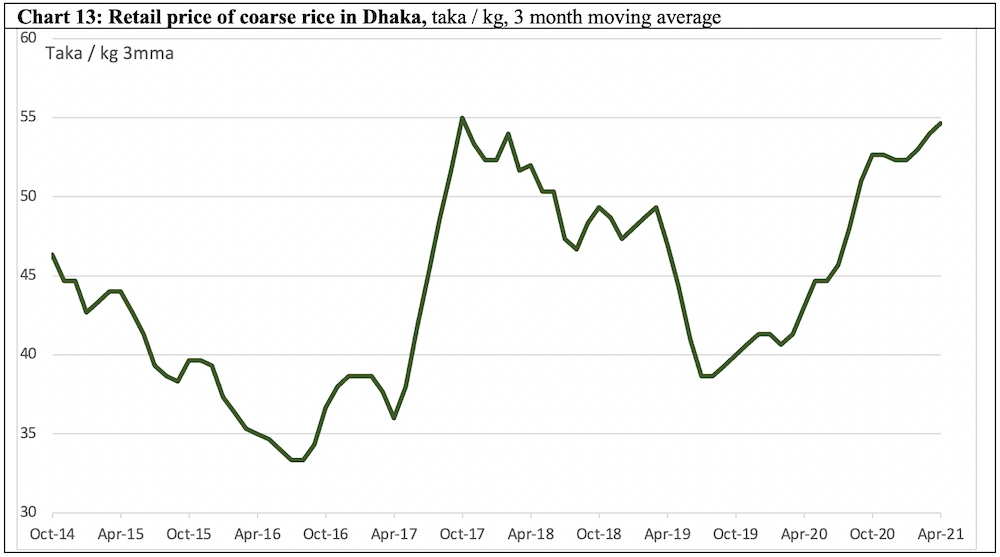

Charts 13 and 14: Price of rice and rental prices in Dhaka

The price of rice continued to rise steadily into April 2021, possibly reflecting the effect of the lockdowns on the supply chain and/or weakness in the agricultural sector. Rental price index in Dhaka meanwhile, showed no sign of recovery as of the spring of 2021.

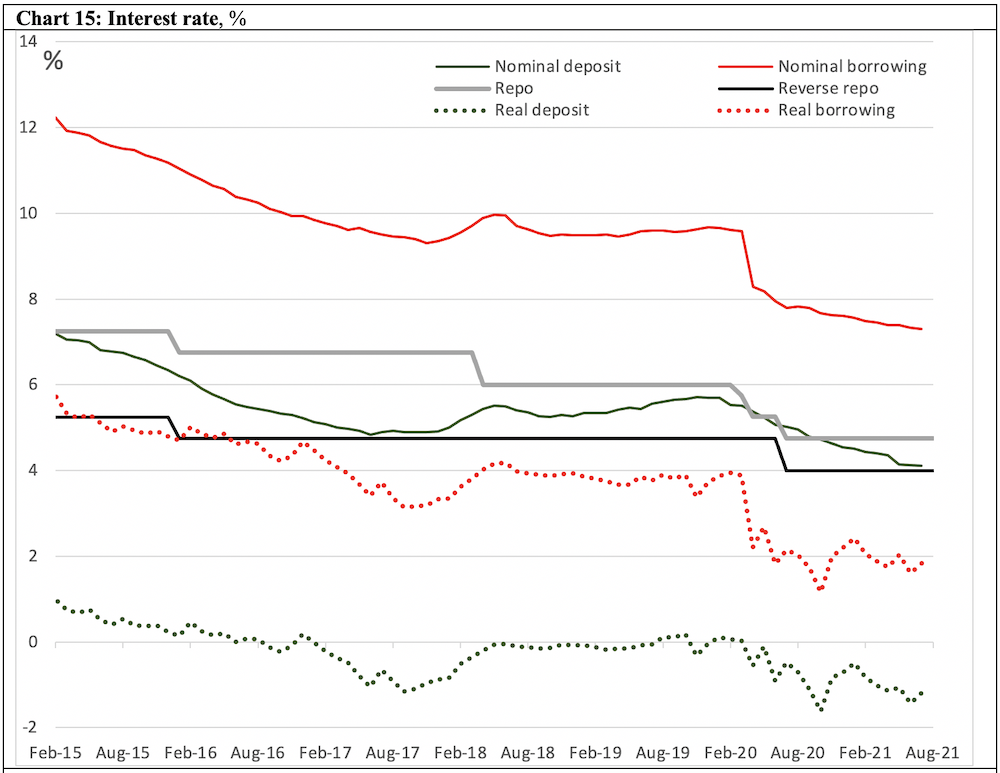

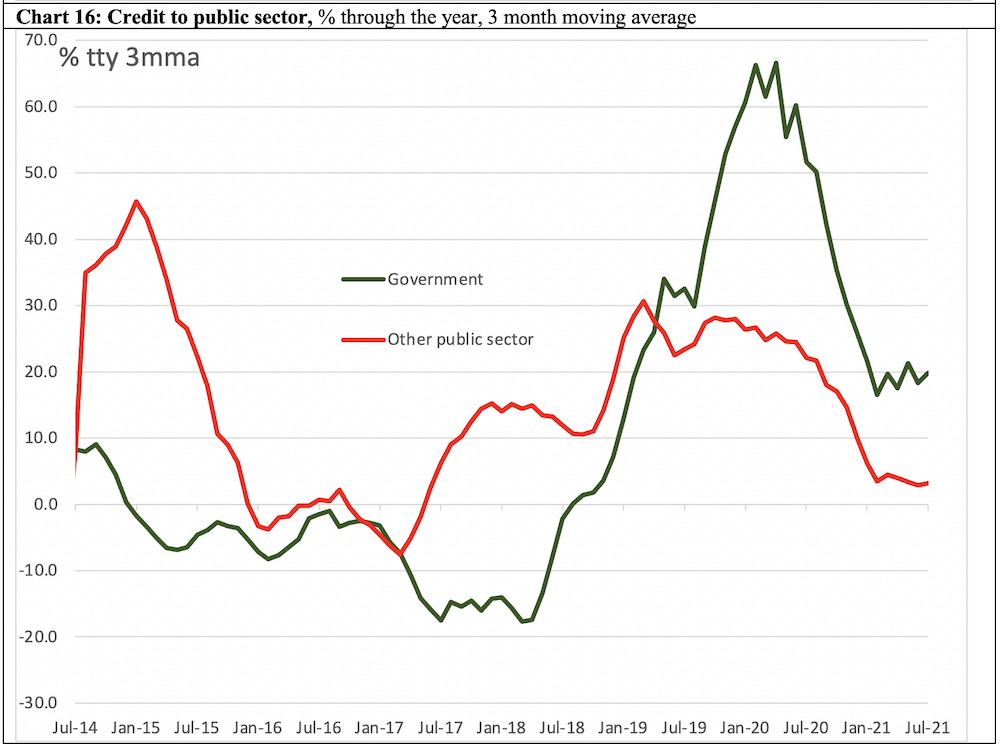

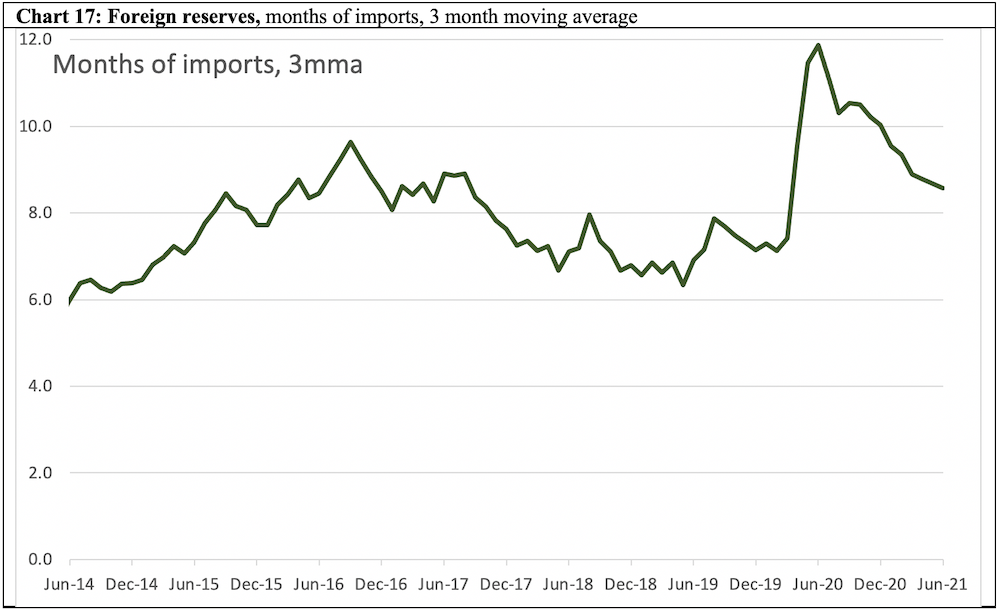

Charts 15, 16, 17: Interest rates, credit to public sector and foreign reserves

Since the beginning of the pandemic, Bangladesh Bank has cut official interest rates, and both deposit and borrowing rates continue to tumble as of August 2021. In theory, this should support economic activities. Public sector borrowing spiked at the onset of the pandemic, but has eased since then. As of June 2021, although Bangladesh Bank’s stock of reserves (expressed in months of imports) has been declining, they continue to be far above what is considered an adequate level (usually said to be 3 months), partly reflecting the collapse in imports shown above.

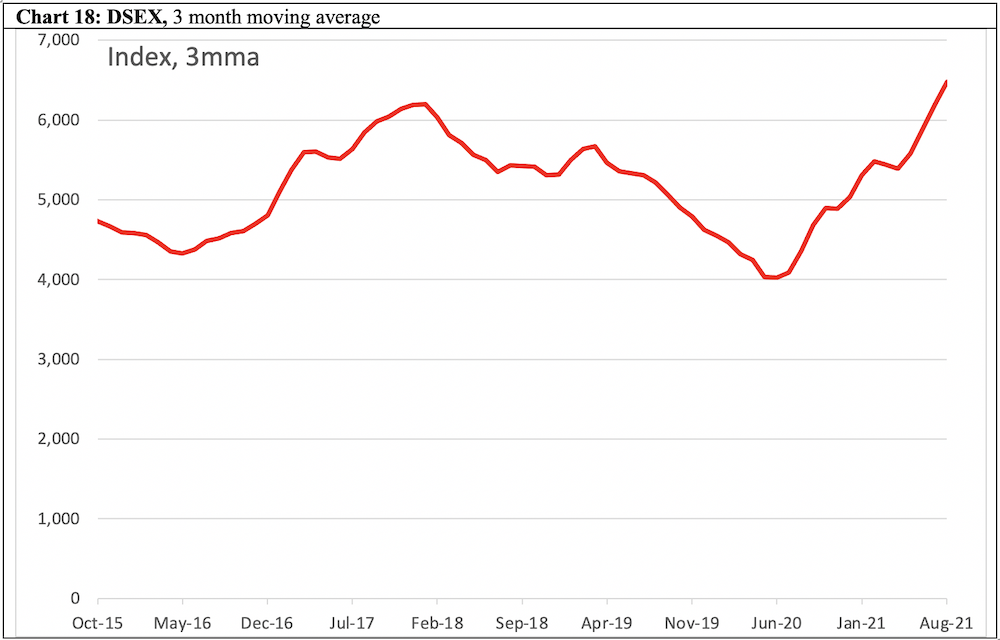

Chart 18: Stock Market

Consistent with many of the indicators above, the Dhaka Stock Exchange (DSEX), which fell from mid-2019, and bottomed out in mid-2020, has been rising steadily to August 2021.

Overall Assessment

Bangladesh economy, already slowing before the COVID-19 recession, was recovering in the summer of 2021, albeit in an uneven manner. Production and external sector indicators recorded the strongest rebound. In contrast, private investment and government expenditure were yet to recover. The early signs point to a further economic slowdown because of the delta variant outbreak, but the full extent of the damage is yet to show up in data. Policies remain supportive of growth. Stock market appears to be optimistic.●

Jyoti Rahman is an applied macroeconomist. His analysis is available at www.jrahman.substack.com.

* All data are from the CEIC Asia Database. Raw data have been smoothed as indicated. The latest available data point in each series is shown in the charts.